The Union Budget 2025 has brought significant changes to India’s income tax structure, raising the question: “Should you opt for the old tax regime versus the new tax regime?”

Whether you’re a salaried professional or a self-employed individual, making the right choice between the old regime vs new regime can help optimize your overall tax liability. This in-depth article explores the new vs the old tax regime slabs and offers key insights to help you decide which tax regime is better for you.

With the Union Finance Minister, Nirmala Sitharaman’s Union Budget 2025 offering a significant income tax relief, particularly no tax burden up to INR 12.75 lakhs – a large segment of the middle-class population in India is able to celebrate joyfully. However, this shift has also led to a key question being raised going forward – Should you move to the new regime, or do the higher deductions and exemptions available under the old regime still offer better overall savings?

The old vs new tax regime 2025 is a topic of constant discussion and picking the one that matches your income range is a matter of careful deliberation. Filing ITR 2026 will become easier if the approach chosen is in sync with your income and expenditure.

How to Choose the Regime?

In technical terms, the most straightforward approach is to total up all the exemptions and deductions that one can possibly claim under the old regime, before deciding which option yields the lowest overall tax liability.

Highlights of the Union Budget 2025

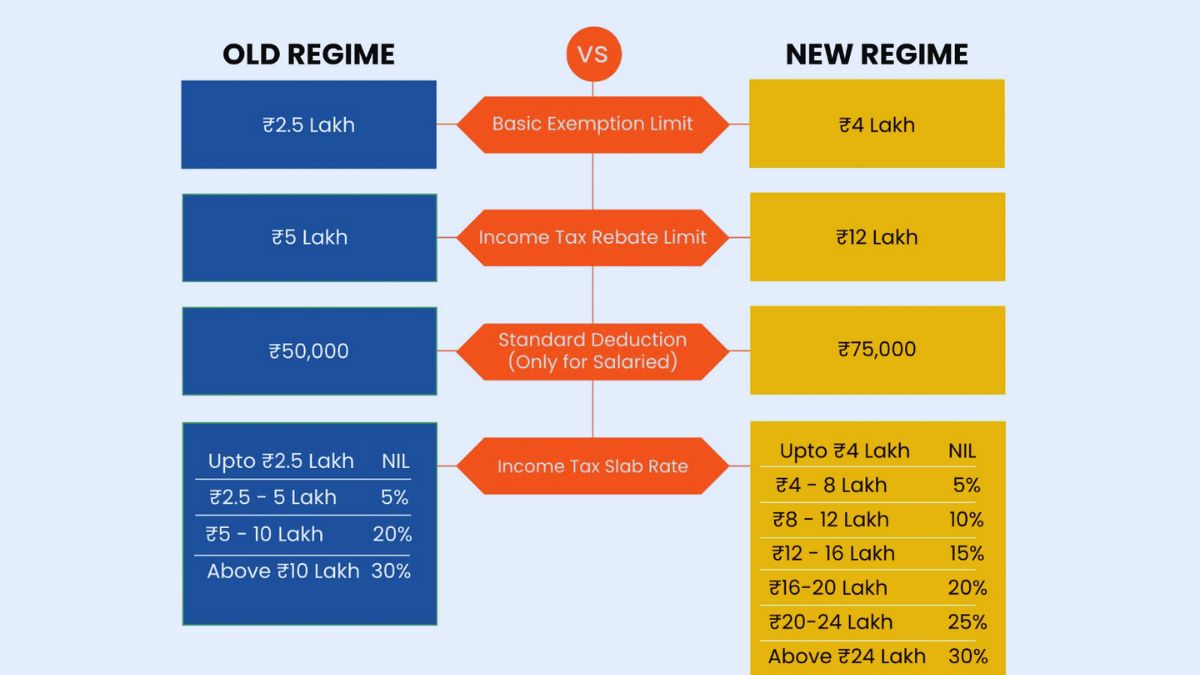

- Under the old regime, taxpayers can still avail of popular deductions (like 80C, 80D, HRA, etc.), whereas the new regime permits fewer exemptions/deductions but provides broader tax slabs and higher exemption thresholds for many.

- As part of the new tax regime, salaried individuals enjoy an additional INR 75,000 standard deduction, effectively raising their zero-tax threshold to INR 12.75 lakhs.

- The new regime largely eliminates conventional tax exemptions and deductions such as HRA, LTA, Section 80C (for investments), and Section 80D (medical insurance).

- The new tax regime has seven major tax slabs, starting with 0% for income up to INR 4 lakhs and rising to 30% for income above INR 24 lakhs.

Difference Between Old vs New Tax Regime

| Criteria | Old Regime | New Regime |

| Basic Exemption Limit | INR 2.5 Lakhs | INR 4 Lakhs |

| Tax Slabs | 5%, 20%, 30% beyond their thresholds | 0%, 5%, 10%, 15%, 20%, 25%, 30% across broader slabs |

| Deductions | HRA, LTA, 80C, 80D, interest on home loan, etc. allowed | Limited (only standard deduction of ₹75k for salaried) |

| Documentation | High (investment proofs, rent receipts, etc.) | Low (fewer deduction claims implies simpler filing) |

| Ideal For which Category | Taxpayers with large deductions & exemptions | Those with limited deductions or prefer simplified slabs |

Who Benefits Most from the Old Tax Regime?

- If you can claim significant deductions – for instance, a minimum of INR 2 lakhs or more through HRA (House Rent Allowance), 80C, 80D, and home loan interest, then the old regime may reduce your taxable income enough to offset the higher tax rates.

- If your total exemptions (HRA, LTA) and deductions (80C, 80D, home loan) are substantial, the old regime could still be beneficial.

- For many in the INR 12 – 20 lakhs’ range, the appropriate regime will depend on how much they have previously invested in the tax-saving instruments.

- Several saving plans to EPF (Employee Provident Fund), Government saving schemes also help in choosing this plan due to more deductions applicable.

- Salaried individuals with substantial HRA (especially in metro cities) or big home-loan interests must adopt the old regime itself.

Who Should Consider the New Regime?

- People who cannot (or prefer not to) invest large sums in instruments like PPF, ELSS, NPS (National Pension Scheme) or insurance solely to save tax.

- High-income earners whose total deductions (excluding the standard deduction) are relatively modest must prefer this approach.

- New tax regime is ideal for those who do not have or cannot utilize large deductions under the old system.

- Salaried individuals up to INR 12.75 lakh who want a zero-tax liability, can opt for this regime.

The exact benefit or loss under the old regime varies with each scenario, reflecting how your exemptions and deductions influences the final result. For every individual, the regime style will change depending on the income bracket, the applicable assets and liabilities and additional income sources that are to be disclosed. For the FY 2025-26 (AY 2026-27), the income tax slabs for old and new regime have been shared above. One must discuss and brainstorm to see all the applicable income sources, deductions and exemptions to fully understand which regime is actually suitable in helping you save more and plan smartly.