It’s a constant thought for every responsible individual to choose the right savings option and aspire for the money to grow more each day. To choose carefully, invest wisely and earn securely through deposit schemes, one must understand the difference between the two most common types of deposit and their benefits.

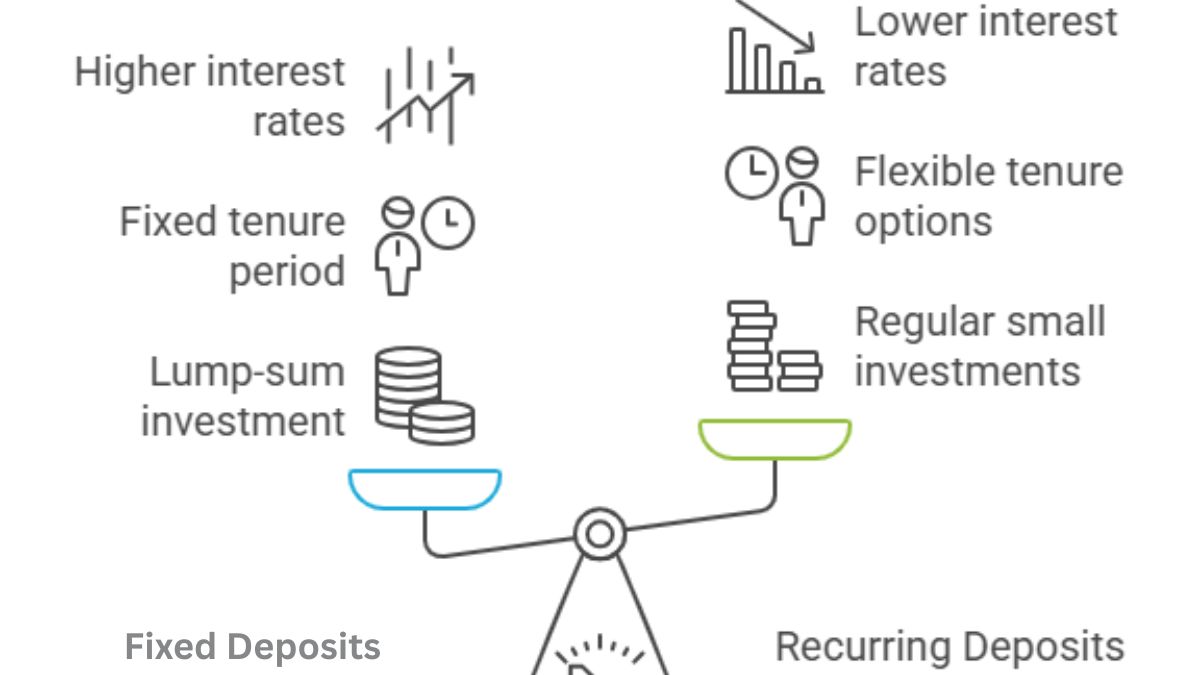

When it comes to making safe and stable investments in India, Fixed Deposits (FDs) and Recurring Deposits (RDs) stand out as two of the most popular choices. Backed by banking companies and offering guaranteed returns, both these instruments suit conservative investors who prefer minimal risk over high but uncertain returns. However, when it comes to opting the better one out of the two, many investors find themselves at a crossroad.

So, in the age-old FD vs RD debate of which is better between the two, the first step begins with assessing the financial goals, analyzing the income pattern and identifying the saving capacity. Let’s break it down to understand which one might work best for you.

Irrespective of the choice one makes between FD and RD, the major benefit which is common to both is that their returns are ensured and are risk-free. The major financial institutions give both RD and FD as fixed income solutions. Both of the schemes allow you to invest a particular amount and receive an interest on that amount. The investors receive the principal amount and the interest at the conclusion of the term period.

What is a Fixed Deposit?

Another name for term-deposit, this is a financial investment product which allows investors to deposit a lump sum amount for a fixed tenure at a fixed interest rate. You deposit a specific amount of money and earn interest on it, which is usually compounded quarterly. At the end of the tenure, you get back your principal plus interest.

Key Features of FD:

- Maturity Period – This can range from a few months to several years and has a fixed period.

- Fixed interest Rate – The interest rates of FDs are fixed and generally higher as compared to regular savings accounts.

- Interest earned on FDs is usually taxable.

- Interest Payout – One can choose to receive their interest payouts periodically (monthly, quarterly, annually) or at maturity.

- Premature withdrawal is allowed by banks but may come with a with penalty charge.

- Banks offer higher interest rates for senior citizens

What is a Recurring Deposit?

The second type of deposit scheme is the Recurring Deposit – which allows an investor to deposit a fixed amount at regular intervals, generally on a monthly basis, for a pre-decided tenure. RDs are a popular way to save money and earn interest over a predefined period.

Key Features of RD:

- Monthly deposits – With an RD, you can deposit a fixed amount of money at regular intervals (usually monthly) for a predetermined period.

- Auto Renewal – Many banks offer an auto-renewal option, where you can reinvest the matured RD amount into a new RD.

- Fixed Term – RDs have a fixed tenure, which can range from a few months to several years. But there are some RDs which may allow to choose the tenure based on your financial goals.

- Interest Rate – The interest rate is generally lower than that of fixed deposits (FDs) but offers more flexibility with respect to the amount to deposit.

How Do the Returns Compare?

As far as an honest comparison between the two types of deposits is concerned, FDs generally offer relatively better interest rates compared to RDs for the same time period. However, because RD contributions are staggered over time, the overall effective return on an RD is lower than that of an FD.

For example, if a bank offers for both FD and RD a 7% interest per annum:

- In FD, the entire amount earns 7% for the full tenure.

- In RD, each monthly installment earns 7% but for varying durations (first installment earns for 12 months, second for 11, third for 10 and so on).

To sum up, a Fixed Deposit has an edge over RD in terms of the total interest earned. However, if an investor wants to inculcate a disciplined and regular saving habit or has financial constraints and cannot allocate a lump sum amount, then Recurring Deposit seems like a more viable choice.

- For a common FD, the interest rate range varies from 3% – 6.85% for regular individuals, while for senior citizens it ranges from 3.50% – 7.35%, depending on the time period selected for the investment.

- In case of a recurring deposit, it ranges from 4.50% – 7.05% for regular citizens, while for the senior residents’ category it goes from 5% – 7.65%, as per the duration opted for.

FD vs RD: Key Differences at a Glance

| Feature | Fixed Deposit (FD) | Recurring Deposit (RD) |

| Investment Type | Single Deposit | Monthly deposit |

| Interest Rate | Slightly higher (generally) | Slightly lower than FDs |

| Liquidity | More liquid (one-time lock) | Less liquid (multiple deposits) |

| Ideal For | People with surplus funds | People with regular monthly income |

| Premature Withdrawal | Possible with penalty | Possible with penalty |

| Senior Citizen Benefit | Available | Available |

| Risk Factor | Low (almost zero) | Low (almost zero) |

Important Tips for Savings

- Tax on Interest – Interest earned from both FD and RD is taxable under ‘Income from Other Sources’ category while filing the returns. If the interest exceeds INR 40,000 (INR 50,000 for senior citizens) in a year, TDS (Tax Deducted at Source) is applicable and deducted by the bank.

- Premature Withdrawal – Both FD and RD allow premature withdrawals, but with a penalty charge. Make sure to align your tenure with your liquidity needs to avoid paying any untoward deduction.

- Inflation Impact – While both are secure modes of deposit schemes, they may not always beat inflation. For long-term goals, consider supplementing them with additional investment options such as mutual funds or equity trading.

- Both FD and RD offer an insurance coverage as a benefit on the deposit amount.

- While investing in FD offers an auto-renewal option, the same is however absent in RD.

Conclusion: FD vs RD – Which is Better?

Fixed Deposits and Recurring Deposits aren’t mutually exclusive or completely independent. Many smart investors use RD to build their savings, then consolidate those savings into a FD once the RD matures. This approach allows them to benefit from both – a regular saving discipline habit and higher FD interest in the long term.

There is no one-size-fits-all answer, but here’s a simplified analogy:

- Choose FD if you have a lump sum amount and want stable, higher returns.

- Choose RD if you want to build savings gradually and are looking for low-risk, disciplined investing method.

Both individually serve different financial purposes. Assess your cash flow, financial goals, and risk appetite before deciding. Or better yet, use a combination of both to balance safety, discipline and returns. You can always speak to a bank professional and seek detailed advice on which one to choose as a more effective deposit scheme.

In a world of volatile market conditions and unpredictable returns, FDs and RDs are like financial comfort pillars—safe, stable, and always reliable. Use them cautiously to create a cushion for your dreams, emergencies, retirement and desires.