Are you tired of feeling like your money disappears before the month ends and you can’t seem to keep a track of where does the money go? Are you someone who is looking for an easy yet effective way to manage your finances without complicated spreadsheets or financial jargon? The stress ends here – as you can now adopt and follow the 50-30-20 budget rule—a tried-and-true method that helps individuals take control of their money, reduce financial complications and helps work toward building solid savings.

This budget rule is the golden matrix one can follow, which serves as a perfect guide to build your savings.

In this article, we’ll break down what the 50-30-20 rule is, how it works, why it’s effective, and how you can start using it right away.

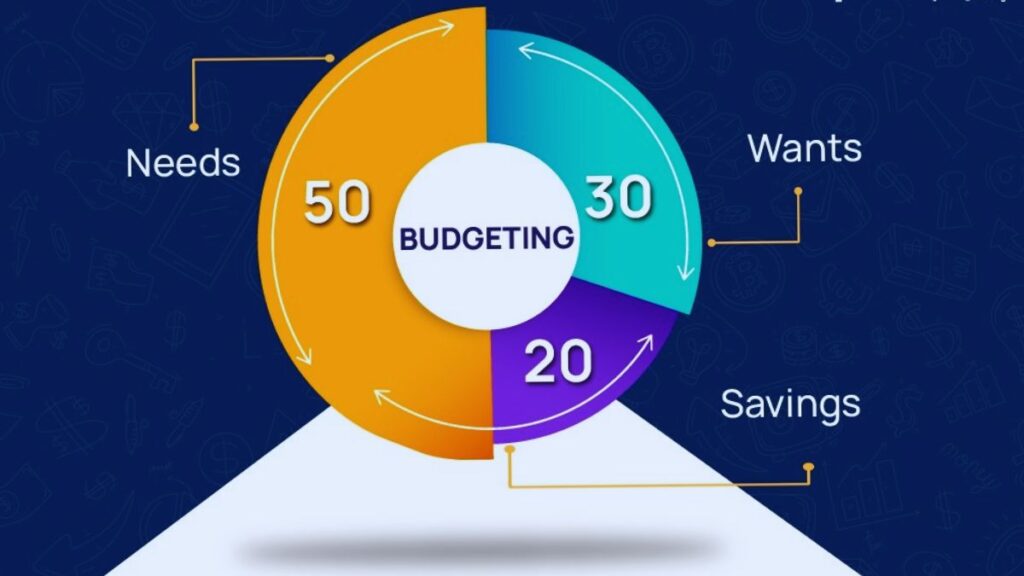

What is the 50-30-20 Budget Rule?

The 50-30-20 rule is a simple budgeting framework that divides your after-tax personal income into three broad categories:

- 50% for Needs

- 30% for Wants

- 20% for Savings and Loan Repayment(s)

This method was initially popularized by U.S. Senate Representative Elizabeth Warren in her book ‘All Your Worth: The Ultimate Lifetime Money Plan’ and has gained global popularity due to its simplicity and effectiveness in utilization.

Let us break the rule into individual components to understand it better.

Breakdown of the 50-30-20 Rule

-

50% – NEEDS

The first category with the maximum share belongs to your ‘Needs’. This portion is reserved for essential expenses one must pay each month to survive and maintain a basic lifestyle. These include:

- Rent or home loan EMI

- Utility bills (electricity, water, gas)

- Food/Clothing – Basic

- Groceries/Ration

- Basic transportation (fuel, public transport)

- Health insurance or medicines

- Loan EMIs (only for essential items – vehicle/education)

Tip: If your needs exceed 50% of your income, consider downsizing or cutting down discretionary expenses to bring it within the recommended range.

-

30% – WANTS

The second chunk of the pie-chart is occupied by ‘Wants’. This category is primarily for the non-essential spending that enhances your lifestyle but isn’t necessary for survival. Some of the examples include:

- Dining out/Recreation

- OTT Entertainment subscriptions

- Additional/Non-Essential Shopping (clothes, accessories)

- Hobbies and entertainment

- Vacations and leisure travel

Tip: Wants can quickly inflate your budget. Track them diligently to avoid any kind of overspending and debt accumulation. The share of this section must not exceed 30% under any circumstances.

-

20% – SAVINGS

The last block belongs to the actual savings section. After deducting the previous two areas that comprise of 80% of the chunk, the final 20% should go towards future financial security, including:

- Emergency fund contributions

- Retirement savings (e.g., PPF, NPS, mutual funds)

- Investments (SIP, stocks, fixed deposits)

- Paying off any credit card bill or personal loans

Goal: You should aim to build an emergency fund with at least 3–6 months’ worth of expenditure secured and start investing early to benefit from interest compounding.

Steps to Follow to Increase Savings

- Calculate Your Net Income – Know your monthly income after tax and deductions, called as the net income. This helps to plan your budget as the first step.

- Track Expenses – Use apps like Walnut, Moneyview, or Excel sheets to track the expenses made under different categories and analyze them accurately.

- Categorize Wisely – You must be able to differentiate between needs and wants clearly. The clear demarcation between categories is of vital importance.

- Automate Savings – You can set up auto-debits for SIPs or RD accounts. This helps to automate your savings and keep unnecessary expense at bay.

- Review Monthly – A periodic review must be carried out to monitor the percentage share being spent and adjust the areas in case there is an increment in the income.

Importance of the 50-30-20 Rule

- Simple & Flexible: Easy for beginners, adaptable for all income levels.

- Encourages Savings: Prioritizes long-term wealth building.

- Prevents Overspending: Sets healthy boundaries on lifestyle expenses.

- Improves Financial Awareness: Helps track where every rupee goes.

How to Implement the Budget Rule?

Here’s a step-by-step guide to using this rule, with for example a monthly take-home salary of INR 60,000/-.

| Category | Allocation | Amount (INR) |

| Needs | 50% | 30,000 |

| Wants | 30% | 18,000 |

| Savings & Repayment | 20% | 12,000 |

As much as the 50-30-20 budget rule has its pragmatic importance and is definitely a functional way to plan your savings, this classical rule may not work in certain cases. While it’s a great starting point, this rule isn’t one-size-fits-all approach-based. You might need adjustments if:

- You live in a metro city with a high cost of living (in some areas the rent may exceed 50% of the earning)

- You have a considerable amount of loan repayments

- You have irregular income (freelancers generally face this)

The 50-30-20 budget rule offers a balanced and beginner-friendly approach to money management. It promotes mindful spending, disciplined saving, and long-term wealth creation. While it might need some tweaking based on your individual circumstances, it’s an excellent starting point for anyone looking to improve their financial health.

After all, right kind if budgeting and saving is all about mindful living.