In India, with a population of over 141 crores, lakhs of citizens apply for loans – personal, vehicle or home loan to meet their requirements, through banking and non-banking finance companies. With more loans, the chances of fraud and financial scams also rise up – with thousands of people not succeeding in returning the borrowed money and ending up as defaulters.

CIBIL, which stands for Credit Information Bureau (India) Limited, is a credit bureau agency that collects and maintains credit information of all individuals and businesses in India. It’s a credit information company that provides credit scores and reports to lenders to help them assess a borrower’s creditworthiness. Essentially, lenders can determine how likely a borrower can repay loans and credit card bills.

CIBIL is now partnered with TransUnion, a US-based company, and is often referred to as TransUnion CIBIL. CIBIL independently was founded in August 2000 and is India’s first credit information association. It acts as a primary credit bureau, trusted by banks and financial institutions to assess a borrower’s creditworthiness. While there are other credit bureaus approved by the RBI, such as Experian, Equifax, and CRIF High mark, CIBIL is the most widely followed in the Indian market.

To begin with, let’s understand what exactly a CIBIL score is – its meaning and how it’s calculated; why it actually matters more than you think.

What is a CIBIL Score?

The CIBIL score, a credit score evaluated by the TransUnion CIBIL, ranges between 300 and 900 and denotes your creditworthiness. A higher score can help you get faster approvals on loans and credit cards. For most banks and non-banking financial companies (NBFCs), a minimum CIBIL score of 700 is preferable.

How is the CIBIL score calculated?

There are various websites and UPI Portals (like Google Pay), that permit free calculation of CIBIL score and indicate the level also. Having a good CIBIL score gives you the leverage while applying for any kind of personal loan, as it portrays the individual as a responsible and trustworthy borrower.

This is primarily because it consolidates the past credit history and repayment behaviour, to present a comprehensive picture to the prospective lenders. A high CIBIL score is indicative of being more creditworthy. CIBIL score is a 3-digit numerical representation ranging from 300 to 900. In this huge range, 900 score is the most ultimate and highest, while 300 marks the lowest. Higher the person’s score, more are the chances of securing an approval on the loan/credit application. In a regular world, a score of around 750 or above is considered ideal to get the loan request affirmed.

To calculate and check your CIBIL score, check out Free CIBIL Score and Report | CIBIL

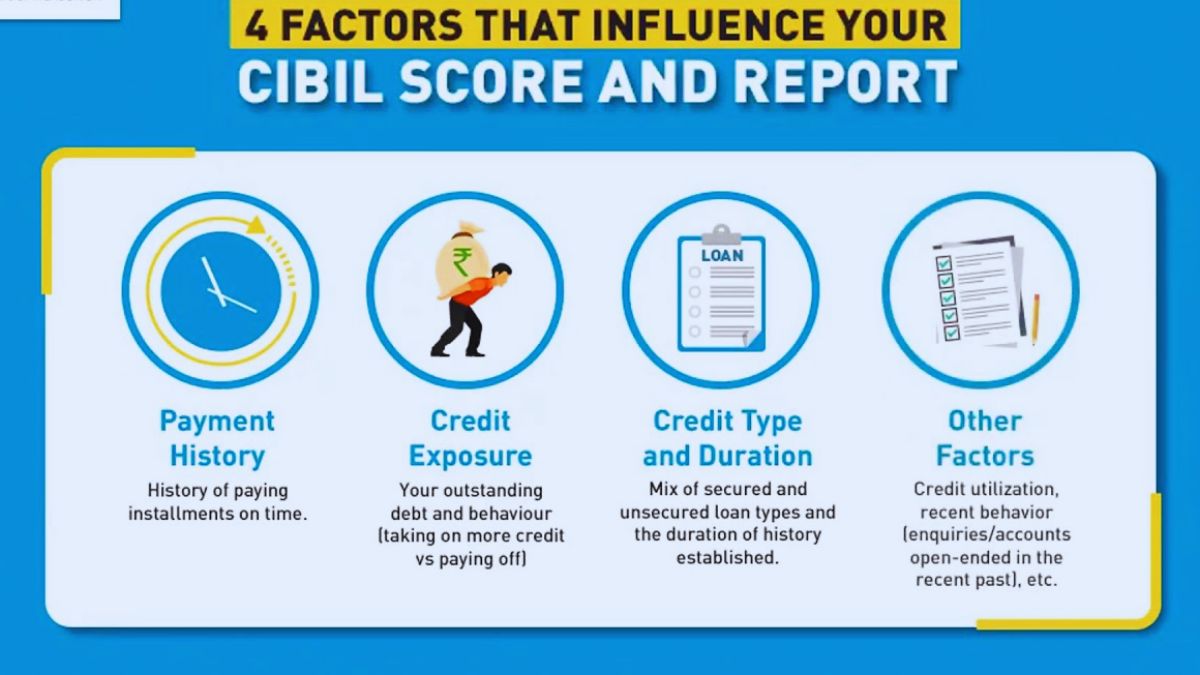

There are four major factors that contribute with some weightage in the calculation of the score.

| Factors | Weightage |

| Repayment History | 30% |

| Credit Exposure | 25% |

| Credit Type & Duration | 25% |

| Other Factors | 20% |

Benefits of a High CIBIL Score

- Enhanced Loan Eligibility

- Less Interest Rates

- Credit Card Benefits

Factors Affecting CIBIL Score

Your CIBIL score is influenced by four main pillars, which primarily decide on the future for seeking credits. Understanding these factors can help maintain a sustainable score and increase the chances of loan approval.

1) Repayment History – Any missed or late EMI payments can significantly impact the score.

2) Credit Utilization Ratio – The CUR measures the amount of credit you have used compared to the total available credit in credit card. Using more than 30% of the credit limit can negatively impact the score. Try to keep the credit utilization ratio results low for better results.

3) Number of Enquiries – Every time you apply for a credit, lenders run through a hard inquiry on your credit report. This is noted in the ‘enquiry’ section of your financial report. However, multiple hard enquiries in a short period can lower your credit score.

4) Credit Age – A longer credit history reflects a more dependable borrower, positively enhancing the score.

What CIBIL Score Should You Maintain for Loans?

- CIBIL gathers sufficient data on all the loan and credit card accounts from banks and other financial institutions.

- Based on this data, CIBIL generates a credit score, which lenders use as a benchmark to evaluate an applicant’s creditworthiness before making a lending decision.

- CIBIL plays a crucial role in India’s financial system by facilitating lending decisions and helping to manage risk.

- For a personal loan approval, having a CIBIL score above 685 is essential. A score of this value and higher suggests fair eligibility and positive sign for approving.

- If your score is above 750, you are seen as a highly reliable borrower and may often receive the most lucrative loan terms available at good interest rates.

- If your CIBIL rating is between 700-749, increasing in higher through lower credit utilization ratio, timely repayments and checking credit reports can result in quicker approvals and competitive offers.

- Keeping your score above the minimum threshold can help the potential candidate to unlock better loan opportunities and manage the finances more effectively.

In essence, your CIBIL score is a financial blueprint that reflects your creditworthiness. By understanding how your repayment history, credit utilization, credit mix, and other factors influence your score, you can take proactive steps to maintain or improve it. A good CIBIL score not only enhances your loan and credit card eligibility but also increases your chances of getting better interest rates and terms, providing significant financial stability.

Moreover, a strong CIBIL score can be advantageous when applying for a personal loan. With a high score, you are more likely to qualify for favorable terms and conditions, offering easier and faster access to funds.

FAQs on CIBIL Score

1) How often should I check my CIBIL score?

You must check your CIBIL score at least twice a year and before you apply for any major loan or credit.

2) What is the minimum CIBIL Score required for a personal loan?

The minimum CIBIL Score requirement for seeking a personal loan depends on the lender. Generally, a score of 700 or above is required, and can enhance your chances of getting approved for a loan with acceptable terms.

3) What is the full form of CIBIL?

The full form of CIBIL is Credit Information Bureau (India) Limited. It was founded in August 2000 and is India’s first credit information association.